In the high-stakes world of deep tech, the “Valley of Death” is more than a metaphor; it is a brutal financial reality.

For years, Indian founders building in quantum computing, semiconductors, robotics, space-tech, or advanced materials faced a frustrating paradox. They needed massive capital to prove their technology worked. The journey from a lab breakthrough to a scalable, market-ready product is long, expensive, and uncertain. But to get capital from traditional venture funds, they usually had to prove the technology already worked and was scaling.

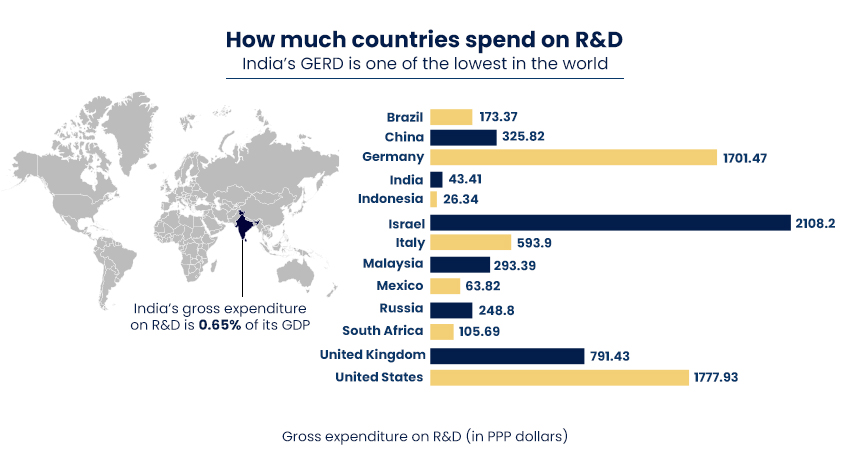

This “chicken-and-egg” problem forced many of India’s brightest minds to either pivot to less ambitious software models or move their headquarters to Silicon Valley or Singapore, where patient capital was more abundant. In 2025, India’s gross expenditure on Research & Development (R&D) stood at a modest 0.64 % of GDP. This is significantly lower than global peers such as China (2.41 %), the United States (3.47 %), and Israel (5.71 %). Meanwhile, the private sector’s contribution was only about 36.4 % of India’s total R&D spend, compared with 70 – 90 % in advanced innovation economies. This disparity has long constrained India’s ability to translate scientific potential into industrial leadership.

Why India’s Deep-Tech Capital Stack Was Broken

Traditionally, deep-tech founders started with research grants from BIRAC or the Department of Science and Technology (DST). These grants helped validate feasibility, but with limit of ₹50 lakh to ₹1 crore, they were sufficient only for lab work, not for pilot plants or for tackling complex global regulations.

The real crisis occurred when technology moved beyond the lab and into engineering. Traditional venture capital (VC) funds typically operate on 7–10-year return horizons. This is fundamentally misaligned with the 12–15-year development cycles common in deep-tech. At the same time, traditional banks require tangible collateral, such as land or machinery. R&D-intensive startups do not have this. Their primary asset is intellectual property (IP), an intangible value that conventional lenders struggle to price. Consequently, as many as 90% of deep-tech projects have historically faltered in this phase due to a lack of capital rather than technical failure.

A clear illustration of this gap is found in semiconductor design. Companies building indigenous chipsets must invest heavily in design, verification, and fabrication before seeing any commercial returns. In 2025, Indian semiconductor startup Netrasemi raised roughly ₹107 crore in Series A funding to advance its AI-powered chips. This is a rare example of capital flowing into early-stage deep-tech hardware.

Union Minister Ashwini Vaishnaw has stressed how such investments enable “Design in India.” Yet cases like this remain rare because the bridge from early design to scaled production has long lacked funding.

Seeing all this, it became clear that without access to long-term patient capital, competing globally was nearly impossible for Indian deep-tech ventures. This structural gap in the middle of the capital stack is exactly what led to the birth of RDIF.

What Is RDIF and Why Does It Matter?

Recognising that the “old” way of funding cannot support the “new” era of deep-tech, the Indian government approved the Research, Development and Innovation Fund (RDIF) on 1 July 2025. Anchored under the Anusandhan National Research Foundation (ANRF), RDIF consolidates a massive corpus of ₹1 lakh crore ($12 billion) to revitalise the innovation economy, with an initial allocation of ₹20,000 crore earmarked for kick-starting operations in FY 2025–26.

What makes RDIF fundamentally different from earlier programs is its intent. It is not structured as a conventional grant scheme. Instead, it is designed as a patient capital platform capable of deploying long-tenor, low- or near-zero-interest loans, equity, and hybrid instruments. The goal is not to replace private capital. It is to make it easier for private investors to participate earlier by absorbing some of the technical and execution risks that previously made deep tech unattractive.

Speaking at industry interactions, Union Minister of State for Science and Technology Dr Jitendra Singh described RDIF as a catalytic mechanism rather than a subsidy, meant to act as an initial push, after which private enterprise and capital markets are expected to scale successful outcomes.

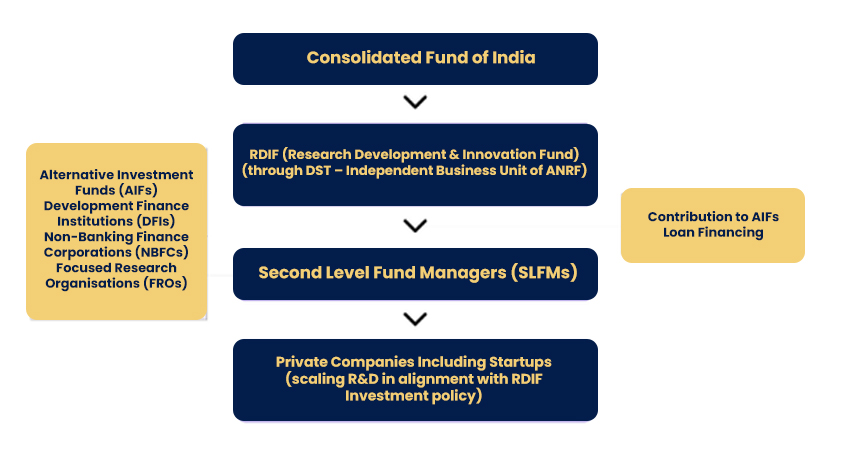

The Layered Architecture: How RDIF Capital Actually Flows

A key strength of RDIF lies in its architecture. Rather than forcing founders to navigate government departments directly, the fund uses a layered deployment model designed to move at market speed while maintaining accountability:

Tier 1: The Custodian (SPF)

A Special Purpose Fund (SPF) under ANRF oversees and manages the ₹1 lakh crore corpus and sets broad strategic policies.

Tier 2: The Disbursers (SLFMs)

Capital is then channelled through Second Level Fund Managers (SLFMs), including regulated Alternative Investment Funds (AIFs), Development Finance Institutions (such as SIDBI), and specialised bodies such as BIRAC and the Technology Development Board (TDB). These entities already understand how to evaluate technology risk and monitor execution.

Applications for SLFMs opened in January 2026. This marked the fund’s operational phase. Now, founders and research-driven companies engage mainly with these professional fund managers, not the government. This structure ensures experts make funding decisions based on technical milestones, not simple checklists.

Turning Fragmented Funding Into a Sequence

The true power of RDIF lies in its ability to create a coherent flow of capital for the founder. Instead of a series of desperate, disconnected fundraising rounds, founders can now navigate a more predictable sequence:

Early Stage (Grants):

Founders can begin with early, non-dilutive grants (like ANRF-ATRI schemes) to achieve lab validation.

The RDIF Bridge (Patient Capital):

This is where RDIF steps in. As technology advances to higher readiness levels, it often requires significant capital for prototyping, pilot manufacturing, and regulatory certification. RDIF-linked financing can then cover a substantial portion—sometimes up to 50%—of assessed project costs. This support dramatically reduces risk at the most capital-intensive stage.

The VC Expansion (Growth Equity):

As RDIF “de-risks” the early technical stages, private VCs are expected to enter with higher confidence. Analysts project that while deep-tech currently accounts for roughly 10 % of India’s startup funding, it could grow to 30 – 50 % over time as this ecosystem matures.

Strategic Sovereignty and Global Ambition

Beyond finance, RDIF is a statement of national strategic intent. The fund prioritises “sunrise and strategic” sectors, quantum computing, robotics, space-tech, AI for agriculture and health, and biomanufacturing, areas where global leadership is determined by who owns the underlying IP. To ensure this value remains in India, RDIF mandates that any intellectual property developed with its support must be owned and registered in India, anchoring long-term economic gains within the domestic economy.

At the World Economic Forum in Davos, Union Minister Ashwini Vaishnaw described India’s shift from aspiration to execution in semiconductors and advanced manufacturing, underscoring the nation’s ambition to build and own core technology platforms.

What This Means For Founders

For founders on the ground, RDIF offers several practical advantages that were previously nonexistent in the Indian market:

- Longer Runways: Founders will gain time to build truly defensible, “deep” technology without pressure to pivot to quick-revenue models.

- Lower Cost of Capital: Low-interest, long-term financing reduces the “burn rate” pressure on their balance sheet.

- Reduced Dilution: Using RDIF debt or hybrid instruments for infrastructure and hardware, founders can preserve more equity for themselves and their team until the company reaches a much higher valuation.

- Institutional Credibility: Backing from the national fund and professional SLFMs sends a powerful signal to global partners and follow-on investors that their technology has been rigorously vetted.

To conclude, RDIF represents a shift from celebrating innovation to systematically financing it. By creating mechanisms to de-risk early innovation and align public capital with private incentives, India is laying the groundwork for a more robust, competitive, and self-reliant deep-tech economy. If implemented effectively, this ₹1 lakh crore patient capital engine could help India move from being a predominantly service-led technology market to one that builds, owns, and exports core intellectual property at a global scale.

For founders, the challenge and opportunity now is clear: sequence capital thoughtfully, build defensible technology, leverage institutional support, and prepare for sustained global competition. For investors, RDIF provides a framework to engage earlier, with greater confidence and co-investment potential, in technologies that were previously too capital-intensive or too slow-burning to underwrite.

The funding engine is now assembled. The responsibility rests on innovators and investors alike to build the technologies worthy of it.